This VBA function and the accompanying Excel spreadsheet calculate the maximum drawdown of a series of investment returns.

The maximum drawdown is the largest percentage drop in asset price over a specified time period.

This article introduces the Stutzer index and provides a calculation spreadsheet. The Stutzer index is an investment performance benchmark that penalizes underperformance against a benchmark.

This Excel spreadsheet demonstrates the classic mean-variance approach for portfolio optimization, but includes the added complication of transaction costs.

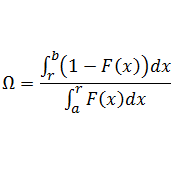

The Omega Ratio can be modified so that it favors return distributions that are skewed to the right with a positive mean, and an exponentially decreasing left-tail. This penalizes dangerous asset behavior which can potentially exist as an edge case.