The 1987 stock market crash had its roots in the misplaced faith the finance industry had in the Black-Scholes framework for option pricing.

Value at Risk with Monte Carlo Simulation

This Excel spreadsheet calculates Value at Risk through the Monte Carlo simulation of geometrical brownian motion in VBA.

Importing Historical Stock Prices from Yahoo into Excel

This Excel spreadsheet imports historical stock prices from Yahoo Finance (http://finance.yahoo.com).

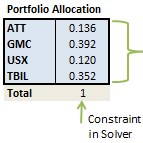

Calculating a Sharpe Optimal Portfolio with Excel

This Excel spreadsheet will calculate the optimum investment weights in a portfolio of three stocks by maximizing the Sharpe Ratio of the portfolio.